The private equity industry has grown dramatically in the last 20 years and we know more than we used to about its effects on the economy.

The private equity industry has grown dramatically in the last 20 years and we know more than we used to about its effects on the economy.

We also know that private equity funds have outperformed public equity markets over the last three decades, even after the fees they charge are accounted for. What have been less explored are the specific actions taken by private equity (PE) fund managers.

PE firms typically buy controlling shares of private or public firms, often funded by debt, with the hope of later taking them public or selling them to another company in order to turn a profit. But how do PE firms decide which companies to buy?

And what do they do once they buy them?

IN A RECENT SURVEY …

In a survey of 79 PE firms managing more than $750 billion in capital, Harvard Business Review provides granular information on PE managers’ practices and how firms’ strategies relate to the characteristics of their founders and do PE investors do what the academics says are “best practices?”

In a survey of 79 PE firms managing more than $750 billion in capital, Harvard Business Review provides granular information on PE managers’ practices and how firms’ strategies relate to the characteristics of their founders and do PE investors do what the academics says are “best practices?”

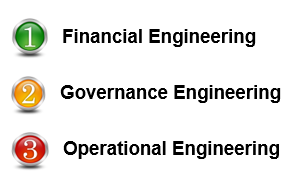

PE firms typically take three types of value increasing actions:

These value-increasing actions are not necessarily mutually exclusive, but it is likely that certain firms emphasize some of the actions more than others. Private equity as defined it in this document does not include venture capital investments.

WHAT’S THE PRIMARY FOCUS OF THIS ENGINEERING? …

WHAT’S THE PRIMARY FOCUS OF THIS ENGINEERING? …

In financial engineering, PE investors provide strong equity incentives to the management teams of their portfolio companies. At the same time, debt puts pressure on managers not to waste money.

In governance engineering, PE investors control the boards of their portfolio companies and are more actively involved in governance than public company directors and public shareholders.

In operational engineering, PE firms develop industry and operating expertise that they bring to bear to add value to their portfolio companies.

WHAT’S THE TARGETED RETURN?

It appears that private equity investors don’t seem to rely on the financial tools taught at business schools. For instance, despite the prominent role that discounted cash flow valuation methods play in academic finance courses, few PE investors use discounted cash flow or net present value techniques to evaluate investments.

It appears that private equity investors don’t seem to rely on the financial tools taught at business schools. For instance, despite the prominent role that discounted cash flow valuation methods play in academic finance courses, few PE investors use discounted cash flow or net present value techniques to evaluate investments.

Rather, they rely on internal rates of return and multiples of invested capital. Instead, PE investors typically target a 22% internal rate of return on their investments on average (with the vast majority having target rates of return between 20 and 25)

An analysis of how private equity firms calculate hurdle rates – the minimum acceptable rate of return on an investment – also indicates also indicates a deviation from what is typically recommended in finance research and teaching.

An analysis of how private equity firms calculate hurdle rates – the minimum acceptable rate of return on an investment – also indicates also indicates a deviation from what is typically recommended in finance research and teaching.

They rely on exit multiples as a shorthand for evaluating their investments. (If a similar company is valued at, say, 10 times its earnings, take the earnings of the company you’ve invested in, multiply it by 10, and you have a rough valuation.)

![]() HBR also asked the PE investors how the funds that provide them with capital – limited partners (LPs) – evaluate their performance.

HBR also asked the PE investors how the funds that provide them with capital – limited partners (LPs) – evaluate their performance.

Surprisingly, the PE investors believe that their LPs are most focused on absolute performance rather than relative or risk-adjusted performance.

AFTER THE INVESTMENT … THEN WHAT?

What happens once PE firms make an investment? The HBR study shows there is evidence of both financial and governance engineering. PE investors say they provide strong equity incentives to their management teams and believe those incentives are very important.

What happens once PE firms make an investment? The HBR study shows there is evidence of both financial and governance engineering. PE investors say they provide strong equity incentives to their management teams and believe those incentives are very important.

They regularly replace top management, both before and after they invest. And they structure smaller boards of directors with a mix of insiders, PE investors, and outsiders. These results are consistent with a focus on value.

Private equity firms founded by financial general partners appear more likely to favor financial engineering and investing with current management. Private equity firms that have founders with private equity experience appear to be the most strongly engaged in operational engineering.

They are more likely to invest with the intention of adding value, to invest in the business, to look for operating improvements, to change the CEO after the deal, and to reduce costs.

Firms founded by general partners with operational backgrounds have investment strategies that fall in between the other improvements, to change the CEO after the deal, and to reduce costs. Firms founded by general partners with operational backgrounds have investment strategies that fall in between the other two groups.

Firms founded by general partners with operational backgrounds have investment strategies that fall in between the other improvements, to change the CEO after the deal, and to reduce costs. Firms founded by general partners with operational backgrounds have investment strategies that fall in between the other two groups.

These results, while preliminary, do seem to indicate that career histories of firm founders have persistent effects on private equity firm strategy. The strategies identified for private equity firms clearly align with the firm founders careers.”

These results, while preliminary, do seem to indicate that career histories of firm founders have persistent effects on private equity firm strategy. The strategies identified for private equity firms clearly align with the firm founders careers.”

Overall, the HBR study confirms the basic strategies PE firms have for adding value to the companies they invest in: aligning incentives, changing management or the governance structure, and looking for operational improvements.

OUR EXPERIENCE CAN HELP …

If you represent a PE firm looking at a company, or a company considering private equity, perhaps our experience on both sides of the equation can be of assistance.

Revitalization Partners specializes in improving the operational and financial results of companies and providing hands-on expertise in virtually every circumstance, with a focus on small and mid-market organizations. Whether your requirement is Interim Management, a Business Assessment, Revitalization and Reengineering or Receivership/Bankruptcy Support, we focus on giving you the best resolution in the fastest time with the highest possible return.